Discover Our Platform: Free Trial for Green Pulse Research Participants

New

Insights

Sustainability Reporting for Non-Listed SMEs: What You Need to Know About VSME

How the EU’s new voluntary standard helps SMEs navigate sustainability reporting more effectively

Sustainability reporting is no longer just for large corporations. As supply chains, investors, and customers push for more transparency, small and medium-sized enterprises (SMEs) are increasingly asked to share their environmental and social performance. But how can SMEs—especially those not covered by mandatory reporting rules—keep up?

Enter the Voluntary Sustainability Reporting Standard for non-listed SMEs (VSME), developed by EFRAG as part of the EU’s SME Relief Package. This post explores what VSME is, why it matters, who it applies to, and how it simplifies sustainability reporting for SMEs.

1. What is VSME?

VSME is a voluntary framework developed by the European Financial Reporting Advisory Group (EFRAG) to support non-listed SMEs in reporting their sustainability performance. It provides a structured, flexible, and proportionate way for SMEs to respond to growing demands for environmental, social, and governance (ESG) data.

VSME is designed to support the availability of simple but relevant sustainability-related data.. It aims at reducing the burden for SMEs currently confronted with multiple uncoordinated data requests and, when supported by the appropriate online platforms and tools, will offer new business and financing opportunities as well as additional management insight to the reporting companies.

2. What is the Purpose of the VSME?

The VSME standard was introduced to:

-

- Reduce the burden of multiple, uncoordinated ESG data requests from various stakeholders.

-

- Provide a simple and practical reporting tool to help SMEs respond to growing sustainability data demands from business counterparties—such as banks, investors, and larger companies.

-

- Support SMEs in accessing sustainable finance by providing a standardized, credible way to report sustainability information that meets investor and lender expectations.

-

- Facilitate the transition to a sustainable economy by promoting market acceptance and providing relevant sustainability-related data.

3. Who can report using VSME?

VSME is designed for undertakings, specifically SMEs, that are not within the mandatory scope of the Corporate Sustainability Reporting Directive (CSRD), but still need to respond to supply chain or investor demands. This includes non-listed micro, small, and medium enterprises that seek to standardize their ESG data reporting to reduce preparation costs and improve access to lenders, investors, and clients.

Although VSME was initially developed for the smallest companies outside the CSRD, a recent development under the EU’s Omnibus proposal expands its relevance. To address the reporting gap for companies with fewer than 1,000 employees that will now fall outside the CSRD scope, the European Commission plans to introduce a voluntary reporting standard based on the VSME framework. This new standard will be adopted through a delegated act.

4. How does VSME differ from other reporting standard?

-

- It’s voluntary, not mandatory

Just like its name, the VSME framework is entirely voluntary. This means that undertakings can engage in sustainability reporting at their own pace, with no legal obligation to comply. In contrast, standards like the European Sustainability Reporting Standards (ESRS) are mandatory for large companies and listed SMEs falling under the CSRD.

-

- “If applicable” principle

One of the key features of VSME is its “if applicable” approach. Undertakings are only expected to report on sustainability data points that are relevant to their operations. If a specific disclosure is not applicable, it can be omitted. When one of these disclosures is omitted, it is assumed to not be applicable. This makes the reporting process more straightforward and significantly less resource-intensive for SMEs.

-

- No double materiality assessment

Unlike ESRS under the CSRD, which requires a comprehensive double materiality assessment, VSME removes this obligation. Double materiality assessments can be complex, resource-intensive, and costly, particularly for SMEs with limited resources. By eliminating this step, VSME significantly reduces the reporting burden, allowing businesses to focus on the sustainability topics that truly matter to them.

5. What’s inside VSME?

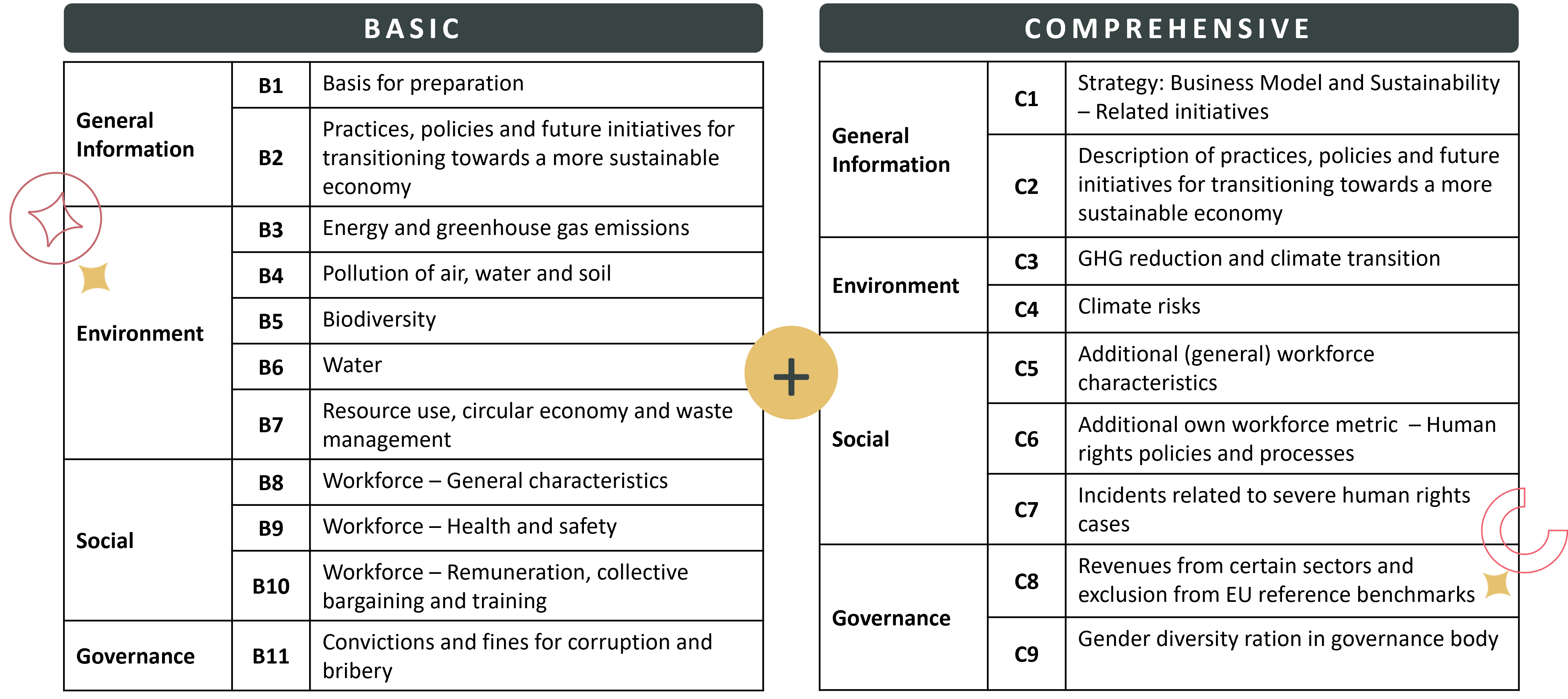

The VSME Standard offers a structured framework for sustainability reporting, organized into two modules that undertakings can use based on their needs and stakeholder expectations.

The Basic Module serves as the core framework and focuses on four key impact areas:

-

- General Information

-

- Environmental Metrics

-

- Social Metrics

-

- Governance Metrics

It contains 11 disclosures and is the starting point for all users of the VSME. Completing the Basic Module is a prerequisite for applying the Comprehensive Module.

The Comprehensive Module builds on the Basic Module with 9 additional disclosures. It is intended for SMEs that need to meet more detailed information requests from banks, investors, and corporate clients. This module covers topics such as:

-

- Business Strategy

-

- Sustainability Policies

-

- Scope 3 Emissions and Emission Reduction Targets

-

- Human Rights

Together, these two modules offer a flexible yet structured approach to sustainability reporting for non-listed SMEs.

6. Getting started with VSME Reporting

To start your reporting journey:

-

- Check the relevancy of VSME to your organization’s size and activities.

-

- Gather the necessary data – Compera can help you identify what kind of data are necessary to report in VSME.

Our application is developed based on VSME and is designed to help SMEs report the data commonly requested by various stakeholders. It offers a user-friendly interface to navigate the disclosure requirements set by VSME. It further provides helpful resources, such as articles, to guide you through the application and the reporting process.

Register as a Professional User and unlock features that go beyond reporting. With the Professional User Plan, you can share the report with other customers, request data from suppliers, and gain a full overview of your supply chain.

Get in touch with us for more detailed information.